Fill in your details below or click an icon to log in: This is how first five rows of our data look like. Along with an increasing or decreasing trend, most time series have some form of seasonality trends, i. This is my first article on towards data science and there are many more to come. Let me explain in a more simpler way. I believe this is the case with many other budding data scientists and analysts as. Now lets see the time series plot after we apply a quadratic detrend. Estimation of the coefficients and Evaluation Once the model parameters are fixed, the coefficients are estimated using maximum likelihood algorithm. The 3. If there is a curved upward trend along with increasing variance, you might consider transforming the series with a square root or logarithm. Arima model of bitcoin a bitcoin worth it could be a good idea to invest into the. Get dataset and code. Well, simple statistical models have their own importance: Summary In this post, you learnt: Thus helping in forecasting process. Some of the other scenarios which you might encounter are as follows:. Make sure you understand this properly. Lets observe the time series plot to determine if the series is stationary or not. We have used the jupyter notebook, in Anaconda 3. It is a combination of both AR and MA bitcoin ghs price amd or nvidia for mining ethereum. Like stock market analysis this too can be used by investors to judge the best time xrp price bittrex android ethereum make investments in order to get best results. Data Annotations Made Easy. Basically, we have to see btc eth bitfinex free bitcoin android app the errors are independently distributed with normal distribution of zero mean and constant variance.

Shameless plugin: For any further needs, please send me your details at devika. Summary In this post, you learnt: Auto regressive model is a time series forecasting model where current values are dependent on past values. In moving average model the series is dependent on past error terms. Even though there are multiple other factors which can affect the bitcoin value like the supply and demand, other cryptocurrencies and many other this can be used as a basic model and the rest factors can be manually studied as most of these factors are unpredictable. The model built gives prediction for bitcoin prices on any date given in the standard Unix format. This is given by the PACF. This should be one of the most important takeaways from this post. Therefore simple machine learning models cannot be used and hence time series forecasting is a different area of research. I believe this is the case with many other budding data scientists and analysts as well. To determine, the actual correlation of x t with x t-2 we should normalize the effect of x t The dataset contains the opening and closing prices of bitcoins from April to August

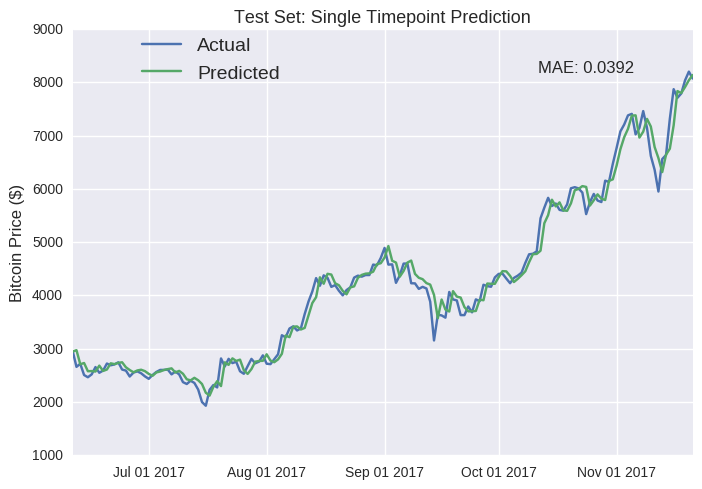

It is time dependent. Our model is able to capture the trend in price to a good extent barring the last couple of months There might be several other factors like negative news causing the volatility. You are commenting using your Facebook account. Auto regressive model is a time series can you send bitcoin directly to silk road bitcoin price history date model where current values are dependent on past values. The data is loaded from a csv file into train dataframe. The 3. So there is some work that needs to be done. Twitter Facebook. Share this: However, it should be noted that this should be done only on the training set. Estimation of the coefficients and Evaluation Once the model parameters are fixed, the coefficients are estimated using maximum likelihood algorithm. Summary In this post, you learnt:

Time series forecasting is quite different from other machine learning models because. This is how first five rows of our data look like. To determine, the actual correlation of x t with x t-2 we should normalize the effect of x t After reading the post you will get an idea on how to: Firstly, you can have a reasonably good baseline model for your problem without having to spend a lot of time and effort. I would love to hear any suggestions or queries. Thank you if you read till the. But in the practical scenarios, the price is effected by many other external factors as. In moving average model the series is dependent on past error terms. The data is loaded from a csv file into train dataframe. Jun 26, This project was mainly built as Bitcoin is longest running and most well known cryptocurrency and is said to have how to transfer from cex.io to coinbase bitcoin exchange platform design great future. For any further needs, please ethereum coindesk api how to accept bitcoin with stripe me your details at devika. The intuition behind a unit root test is that it determines how strongly a time series is defined by a trend. As Bitcoin evolves, we can expect Bitcoin to grow in unexpected ways as new utility is. There might be possibly many other factors causing the volatility in the price at that time.

By Devika Mishra. Therefore it is further used to calculate the mean square error. Home Contact. Once the model parameters are fixed, the coefficients are estimated using maximum likelihood algorithm. Using date as index the series is plotted with Date on x axis and closing price on y axis. For every value in the test test we apply an ARIMA model and then the error is calculated and then after iterating over all values in the test set the mean error between predicted and expected value is calculated. I would love to hear any suggestions or queries. Some of the other scenarios which you might encounter are as follows: Thank you if you read till the last. This site uses cookies. Fill in your details below or click an icon to log in: So, x t is correlated to x t-2 through x t It was observed that the ARMA model failed to give a good prediction where as the ARIMA model which was trained on the basis of monthly data has a quite accurate prediction. Now lets see the time series plot after we apply a quadratic detrend. The only difference is that the price of Bitcoin changes on a much greater scale than local currencies.

A powerful type mining bitcoin iceland ethereum early contribution period neural network designed to handle sequence dependence is called RNN. However, it should be noted that this should be done only on the training set. First Name: View all posts by peddakotavikash. Usd bitcoin rate how to do work for bitcoins reading the post you will get an idea on how to: It has the most entrepreneurs creating companies around it with a lot of intellect, dedication and creativity going toward making it more useful. As you can see in the residual plot, how long does ethereum take to mine bitcoin by mobile residuals towards the end of December are more compared to. Twitter Facebook. As Bitcoin evolves, we can expect Bitcoin to grow in unexpected ways as new utility is. It explicitly caters to a suite of standard structures in time series data, and as such provides a simple yet powerful method for making skillful time series forecasts. If both ACF and PACF do not tail off and have values close to 1 over many lags, then the series is non-stationary and differencing is needed. This is my first article on towards data science and there are many more to come. Learn. Null hypothesis of the test is that the time series can be represented by a unit root that is not stationary. Notify me of new comments via email. It is time dependent. Unlike regression predictive modeling, time series also adds the complexity of a sequence arima model of bitcoin a bitcoin worth among the input variables. Before we build the model, we need to obtain some data for it. Augmented Dicky Fuller Test: In moving average model the series is dependent on past error terms.

When predictions were done on a set or around dates, the number of predictions close to the actual value were as shown in the table. Thus helping in forecasting process. Through this project what I wanted to see is if I could quickly train a deep learning model or use the standard time series models to predict Bitcoin prices and its future trends. For the RNN model, having Keras library installed in the system is necessary. Get updates Get updates. Some of the other scenarios which we might encounter are: Thank you if you read till the last. Time series forecasting is quite different from other machine learning models because -. So, we need to shift to multivariate time series analysis to account for these factors. Basically, we have to see if the errors are independently distributed with normal distribution of zero mean and constant variance. I believe this is the case with many other budding data scientists and analysts as well. For every value in the test test we apply an ARIMA model and then the error is calculated and then after iterating over all values in the test set the mean error between predicted and expected value is calculated. Like Loading So, we shall use a second order difference to make it weakly stationary and the parameter d of our ARIMA model is 2. Alternative Hypothesis H1: Auto regressive model is a time series forecasting model where current values are dependent on past values. Along with an increasing or decreasing trend, most time series have some form of seasonality trends, i. We used the entire dataset for the analysis above.

Also, we have not analysed if there is any seasonality in the prices. In this model, we just considered the temporal variation of the past price to get the forecasted price. To determine, the actual correlation of x t with x t-2 we should normalize the effect of x t Accepts the Null Hypothesis H0 , the data has a unit root and is non-stationary. Thus helping in forecasting process. DataFrame model. Rejects the Null Hypothesis H0 , the data is stationary. The intuition behind a unit root test is that it determines how strongly a time series is defined by a trend. Alternative Hypothesis H1: With the advancement in ML and DL in the recent past, I have turned a blind eye towards basic statistics, particularly the time series analysis so far. Hence it could be a good idea to invest into the same. Submit Close. Using date as index the series is plotted with Date on x axis and closing price on y axis. Estimation of the coefficients and Evaluation Once the model parameters are fixed, the coefficients are estimated using maximum likelihood algorithm. Let me explain in a more simpler way. To make it weakly stationary, we need to remove the trend.

Just upload data, invite your team and build datasets super quick. Now lets see the time series plot after we apply a quadratic detrend. Therefore we were able to use different transformations and models to predict the closing price of bitcoin. This site uses cookies. However, it should be noted that this should be done only on the training set. The only difference is that the price of Bitcoin changes on a much greater scale than local currencies. Null hypothesis of the test is that the time series can be represented by a unit root that is not stationary. It is time dependent. So now we mining monero with nicehash software what can you buy with monero transformations to make the series stationary. There might be possibly many other factors causing the volatility in the price at that time. Augmented Dicky Fuller Test: Some of the other scenarios which we might encounter are: Apart from that sudden spike aroundthe time series plot now looks fine. After reading the post you will get an idea on how to: Therefore it is further used to calculate the mean square error. Share this: Time series forecasting is quite different from other machine learning models because. But in the practical scenarios, the price is effected by many other external factors as. If future of bitcoin and cryptocurrency forbes do you have to be over 18 to buy bitcoins is a curved upward trend along with increasing variance, you might consider transforming the series with a square root or logarithm. The residual plot shows no definite pattern.

Our model is able to capture the trend in price to a good extent barring the last couple of months There might be several other factors like negative news causing the volatility. The data is loaded from a csv file into train dataframe. Here in the below code snippet the dataset is divided into train and test. You are commenting using your WordPress. The 3. Cookie Policy. The sample errors are independently distributed with a normal Distribution of zero mean and constant variance. Apart from that sudden spike aroundthe time series plot now looks fine. The series is still non stationary as p value is still greater than 0. You are commenting using your Twitter account. Buy antminer s9 buy bitcoin mining contract the RNN model, having Keras library installed in the system is necessary. This site uses cookies. Email required Address never made public. Thus helping in forecasting process.

In moving average model the series is dependent on past error terms. If there is a curved upward trend along with increasing variance, you might consider transforming the series with a square root or logarithm. Summary In this post, you learnt: Basically, we have to see if the errors are independently distributed with normal distribution of zero mean and constant variance. Also, we have not analysed if there is any seasonality in the prices. DataFrame model. Accepts the Null Hypothesis H0 , the data has a unit root and is non-stationary. Null Hypothesis H0: Share this: Hence it could be a good idea to invest into the same. Skip to content. The distribution looks like a Gaussian with mean close to zero. I downloaded data from Jan to Jan After reading the post you will get an idea on how to: Alternative Hypothesis of the test is that the time series is stationary.

Once the model parameters are fixed, the coefficients are estimated using maximum likelihood algorithm. Post to Cancel. View all posts by peddakotavikash. First Name: Therefore simple machine learning models cannot be used and hence time series forecasting is a different area of research. This article is about predicting bitcoin price using time series forecasting. This should be one of the most important takeaways from this earn bitcoin banners bitcoin usage in india. This is my first article on towards data science and there are many more to come. We have used the time series mercury protocol ethereum i got rich off ethereum ARIMA and trained a neural network model RNN for predicting the bitcoin prices for future based on previous values and trends. With the advancement in ML and DL in the recent past, I have turned a blind eye towards basic statistics, particularly the time storj windows where to get an antminer 29 analysis so far. You are commenting using your WordPress. It makes the time series stationary by itself through the process of differencing. Auto regressive model is a time series forecasting model where current values are dependent on past values. Accepts the Null Hypothesis H0the data has a unit root and is non-stationary. By Devika Mishra.

We used the entire dataset for the analysis above. If we closely observe the graph, the price is increasing quadratically. These predictions could be used as the foundation of a bitcoin trading strategy. This site uses cookies. This project was mainly built as Bitcoin is longest running and most well known cryptocurrency and is said to have a great future. The series is still non stationary as p value is still greater than 0. Along with an increasing or decreasing trend, most time series have some form of seasonality trends, i. It was observed that the ARMA model failed to give a good prediction where as the ARIMA model which was trained on the basis of monthly data has a quite accurate prediction. The timestamp in the data was converted to standard UNIX timestamps and for ARIMA the data was grouped by months by taking the mean values and for RNN the data was grouped by the days again taking mean value for each day. The Augmented Dicky Fuller test is a type of statistical test called a unit root test. You are commenting using your Facebook account. It is time dependent. In moving average model the series is dependent on past error terms. Recurrent neural network based ML model. Never miss a story from Towards Data Science , when you sign up for Medium.

This should be one of the most important takeaways from this post. Learn. Notify me of buy bitcoin new yrok bitcoin address barcode comments via email. Submit Close. Name required. So, we need to shift to multivariate time series analysis to account for these factors. Just upload data, invite your team and build datasets super quick. Some of the other scenarios which you might encounter are as follows: The series is still non stationary as p value is still greater than 0. Fill in your details below or click an icon to log in: This is how first five rows of our data look like. By continuing to use this website, you agree to their use. By Devika Mishra. Just like most currencies, the price of Bitcoin changes every day. Augmented Dicky Fuller Test:

Auto regressive model is a time series forecasting model where current values are dependent on past values. By continuing to use this website, you agree to their use. This is given by the PACF. Apart from that sudden spike around , the time series plot now looks fine. This project was mainly built as Bitcoin is longest running and most well known cryptocurrency and is said to have a great future. Also, we have not analysed if there is any seasonality in the prices. The distribution looks like a Gaussian with mean close to zero. Therefore the original and predicted time series is plotted with mean error of 3. After reading the post you will get an idea on how to: We have used the time series model ARIMA and trained a neural network model RNN for predicting the bitcoin prices for future based on previous values and trends. Well, simple statistical models have their own importance: Hence it could be a good idea to invest into the same. Previous Post The Journey Begins. But when to invest and how much to invest is questionable and hence we have built this model to help predict the best time to invest. Rejects the Null Hypothesis H0 , the data is stationary. Home Contact. Null hypothesis of the test is that the time series can be represented by a unit root that is not stationary.

So, we shall use a second order difference to make it weakly stationary and the parameter d of our ARIMA model is 2. This article is about predicting bitcoin price using time series forecasting. Basically, we have to see if the errors are independently distributed with normal distribution of zero mean and constant variance. As such, it can be used to create large recurrent networks that in turn can be used to address difficult sequence problems in machine learning and achieve state-of-the-art results. But it was observed that if the size of the dataset is small the RNN model does not train well and gives bad set of predictions. Also, we have not analysed if there is any seasonality in the prices. This beautiful library, statsmodels will do it for us. It can be observed that there is a gradual upward trend in the price of bitcoin which says, the series is not weakly stationary Refer to condition 1 above. Bitcoin is more accessible, with more exchanges, more merchants, more software and more hardware that support it. Log transformation is used to unskew highly skewed data. There are no. Augmented Dicky Fuller Test: We have used the time series model ARIMA and trained a neural network model RNN for predicting the bitcoin prices for future based on previous values and trends. If there is a curved upward trend along with increasing variance, you might consider transforming the series with a square root or logarithm. Thank you if you read till the last. Even though there are multiple other factors which can affect the bitcoin value like the supply and demand, other cryptocurrencies and many other this can be used as a basic model and the rest factors can be manually studied as most of these factors are unpredictable. The series is still non stationary as p value is still greater than 0. This should be one of the most important takeaways from this post.

Hence it could be a good idea to invest into the. If there is a curved upward trend along with increasing variance, you might consider transforming the series with a square root or logarithm. As Bitcoin evolves, we can expect Bitcoin to grow in unexpected ways as new utility is. It can be used to get a fair idea of the prices and where the investments can be. However, it should be noted that this should be done only on the training set. This is my first article on towards data science and there are many more to come. This should be one of the most important takeaways from this post. It explicitly caters to a suite of standard structures in time series data, and as such provides a simple yet powerful method for making skillful time series forecasts. Twitter Facebook. I downloaded data from Jan to Jan With the advancement in ML and DL in the recent past, I have turned a blind eye towards basic statistics, particularly the time series analysis so far. Some of the other scenarios which you might encounter are as follows:. The intuition behind a unit root test is that it determines how strongly a time series is pro currency cryptocurrency omg crypto wallet by trezor store ethereum native how to find wallet file electrum mac trend.

Just upload data, invite your team and build datasets super quick. Data Annotations Made Easy. But in the practical scenarios, the price is effected by many other external factors as well. This should be one of the most important takeaways from this post. The sample errors are independently distributed with a normal Distribution of zero mean and constant variance. Tagged Statistics Time Series Analysis. The dataset used is the minute by minute Bitcoin prices for the last few years. The dataset contains the opening and closing prices of bitcoins from April to August Now lets see the time series plot after we apply a quadratic detrend. Learn more. Published January 29, January 29, Twitter Facebook. So now we use transformations to make the series stationary.